The rollout of B2B electronic invoicing in Europe is accelerating under the influence of several regulations (European Directive 2014/55/EU, ViDA initiative, etc.), making this change an opportunity to modernize and secure business transactions. Conversely, ignoring this regulatory wave exposes you to major financial risks (penalties, late payments) and a decline in competitiveness.

In 2026-2027, several countries will take a key step, marking the gradual end of paper and PDF formats in favor of structured formats. This article presents the deadlines for B2B e-invoicing in the following six countries: Germany, Belgium, Denmark, Spain, France, and Greece.

Germany: A Gradual Transition Until 2028

The Growth Opportunities Act (Wachstumschancengesetz, 2024) introduces a phased e-invoicing obligation for German businesses.

Permitted formats

Standard-compliant EN16931 formats that will be accepted:

- XRechnung

- ZUGFeRD 2.3

- Other EDI formats, subject to mutual agreement between trading partners.

No centralized national platform

Businesses will have to rely on:

- Existing networks such as Peppol (which is highly recommended).

- Service providers capable of converting, transmitting, and receiving invoices.

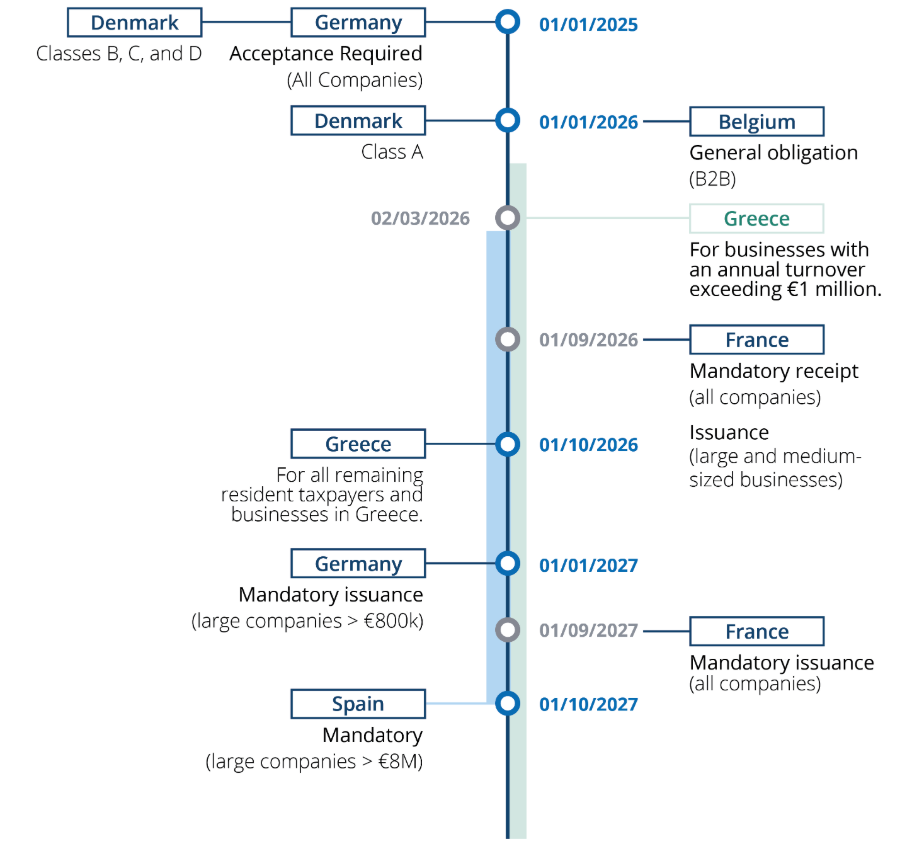

B2B Implementation Timeline

| Date | Obligation | Applies To |

| January 1, 2025 | Businesses must be able to receive EN16931-compliant invoices. | All businesses |

| January 1, 2027 | Paper and PDF invoices can no longer be issued. | Companies with annual revenue above €800,000 |

| January 1, 2028 | All invoices must be issued electronically. | All businesses |

Technical implications for businesses

- To comply with the requirements to receive structured electronic invoices from 2025.

- Adapt their ERP and accounting systems to generate and send invoices in XRechnung or ZUGFeRD formats.

- Choose a transmission channel (Peppol, service providers, EDI, etc.)

- Guarantee the legal archiving of invoices for 10 years.

Belgium: A Model Aligned with Peppol

The law of 6 February 2024 makes electronic invoicing mandatory from 1 January 2026 for all domestic VAT-registered B2B transactions.

Formats and transmission

- Format: Peppol BIS 3.0, EN16931 compliant.

- Transmission: Via the Peppol network is strongly recommended.

E-Reporting and ViDA (VAT in the Digital Age) initiative

Belgium plans to implement near-real-time e-reporting by 2028, based on a five-corner model, in compliance with the European ViDA directive.

Archiving

Electronic invoices must be kept for 7 years.

Denmark: Towards 100% Digital Accounting

Although B2B e-invoicing is not mandatory, the Bookkeeping Act of May 2022 requires digital bookkeeping for businesses.

Bookkeeping Act (May 2022)

This legislation imposes new obligations on digital bookkeeping:

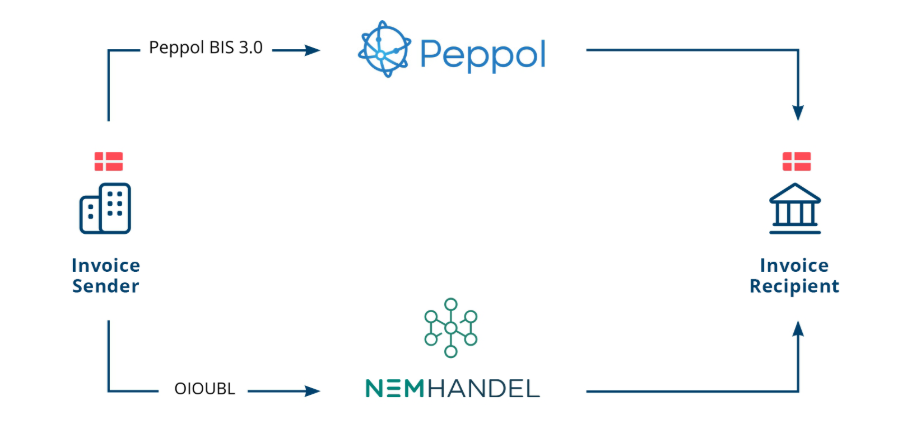

- The mandatory use of certified systems capable of generating, receiving, processing, and archiving electronic invoices in accepted formats.

- Connection to the Peppol and NemHandel networks is required.

Implementation timeline

| Date of application | Businesses concerned |

| January 1, 2025 | Businesses that are required to submit an annual report (Classes B, C, and D) and that do not have certified systems. |

| January 1, 2026 | Other enterprises (class A) that do not submit an annual report to the ERST, whose turnover exceeds DKK 300,000 over two consecutive financial years, and that use an unregistered system. |

Accepted formats

The formats accepted in Denmark are:

- Peppol BIS 3.0

- OIOUBL 3.0 (cancelled by the government)

- OIOUBL 2.0/2.1: Remains active during the transition period.

- NemHandel BIS 4: (Based on Peppol BIS 4 + Danish national extensions) The new target format, expected to roll out in 2028 and fully replace all OIOUBL formats by mid-2029

Archiving

The legal retention period for invoices is 5 years.

Spain: A Schedule Still to be Confirmed

The “Crea y Crece” Law (2022) establishes phased mandatory B2B electronic invoicing. The implementing decree, which is awaiting publication, will set the timeline.

Provisional schedule

The initial timeline, which may be subject to adjustment depending on the publication of the technical regulations, is as follows:

| Business Category | Deadline for application | Estimated adoption date |

| Large businesses (annual turnover > €8 million) | 1 year | October 2027 |

| SMEs and other businesses (turnover < €8 million) | 2 years | By 2028 at the latest |

Accepted formats

The electronic invoice formats that will be accepted are as follows:

- UN/CEFACT CII (XML)

- UBL (XML)

- EDIFACT

- Facturae

Spanish B2B e-invoices must comply with the European e-invoicing standard EN 16931.

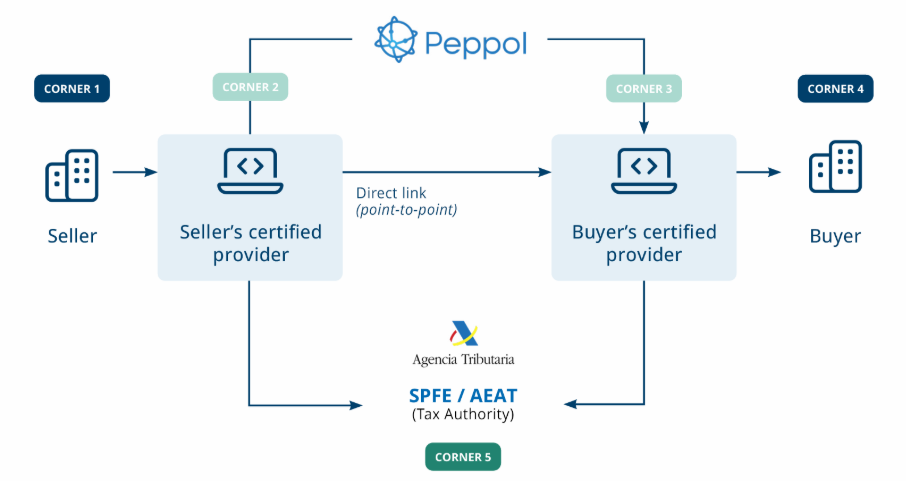

Exchange platforms

The platforms intended by the reform are as follows:

- The SPFE (Solución Pública de Facturación Electrónica) is Spain’s new public e‑invoicing platform, managed by the AEAT, designed to support the mandatory B2B e‑invoicing system. It will act as a central reporting and repository solution alongside private interoperable platforms. It is expected to be operational by August 2027. It does not formally replace FACeB2B, and FACe remains in use for B2G invoicing.

- Interoperable private platforms (5-corner model): Businesses can choose certified private service providers. Similar to the French model, these certified platforms are freely interoperable with one another, while securely connecting and reporting data directly to the SPFE.

E-Reporting

Two systems coexist:

- Suministro Inmediato de Información (SII): the near real-time transmission of data to the AEAT (Spanish Tax Administration) for large businesses (turnover > €6 million) and those subject to the monthly REDEME VAT regime.

- Veri*Factu: applicable from 2027 to all businesses not subject to the SII.

Archiving

Invoices must be kept for 6 years, and a tax audit period is 4 years.

France: Approved Platforms and Fixed Deadlines

France will adopt a 5-corner model, centered around the Public Invoicing Platform (PPF) acting as a data collection hub, along with certified platforms (Plateforme Agréée – PA).

Implementation timeline

The e-invoicing obligation will gradually apply to businesses:

- Reception: mandatory for all businesses from September 2026.

- Issuance:

- September 2026: Large and mid-sized companies

- September 2027: small and medium-sized enterprises (SMEs) and micro-enterprises.

Architecture – 5-Corner Model

Since the announcement of October 15, 2024, businesses will no longer be able to exchange invoices directly through the Portail Public de Facturation (PPF). They will have to use Plateforme Agréée (PAs) (formerly PDPs) for the transmission of invoices and the reporting of data to the tax authorities, and the Chorus Pro portal will continue to be used for the public sector.

The PPF will only have the role of collecting and aggregating data for the tax administration (“Concentrateur De Données,” CDD).

E-Reporting

E-reporting will apply to:

- B2C transactions

- Non-domestic transactions (intra-EU and extra-EU)

Accepted Formats

Only three e-invoicing formats will be accepted:

- UBL

- UN/CEFACT CII

- Factur-X

Archiving

The minimum retention period for invoices is 10 years according to the Commercial Code. For tax purposes (CGI), it is 6 years.

Greece: Mandatory B2B E-Invoicing Starting 2026

Greece has obtained authorization from the European Commission to make B2B e-invoicing mandatory.

Timing and scope of the B2B obligation

- March 2, 2026: For businesses with an annual turnover exceeding €1 million.

- October 1, 2026: For all remaining resident taxpayers and businesses in Greece.

The obligation will apply only to taxable persons established in Greece.

Integration with the myDATA system

The data from B2B electronic invoices will have to be reported directly and automatically to the myDATA platform in real time.

Archiving

Invoices and accounting data transmitted via myDATA must be archived for a minimum period of 5 years.

For businesses operating internationally, knowing the deadlines and models specific to each country is essential for ensuring tax and operational compliance.