- What is Making Tax Digital (MTD)?

- What is UK E-Invoicing?

- Who is in Scope for the 2029 Mandate?

- The UK’s E-Invoicing Foundation: Directive 2014/55/EU?

- The UK E-Invoicing Mandate Timeline: A Complete Roadmap to 2029

- The Model Behind the Mandate: The Decentralized “4-corner” Model

- How to Prepare for the UK E-Invoicing Mandate Before 2029

- Future-Proof Your E-Invoicing with Symtrax

- FAQs

What is Making Tax Digital (MTD)?

The UK tax system is changing, and HMRC is driving that change. They are moving businesses away from manual tax processes toward a fully digital system. That initiative is called Making Tax Digital (MTD). It is HMRC’s long-term plan to modernize the UK tax system, reduce errors, improve accuracy, and make financial reporting more efficient for businesses of every size. MTD for VAT is already live.

The next big step in this journey is the UK e-invoicing mandate.

What is UK E-Invoicing?

UK e-invoicing means replacing PDFs and paper invoices with structured, machine-readable invoices that flow directly between accounting systems without manual intervention. In November 2025, the UK government confirmed this will become mandatory for all VAT-registered businesses from 1 April 2029.

If you are new to the concept, read our guide on what e-invoicing is and how it impacts businesses before diving into the UK e-invoicing mandate.

What has the UK confirmed so far?

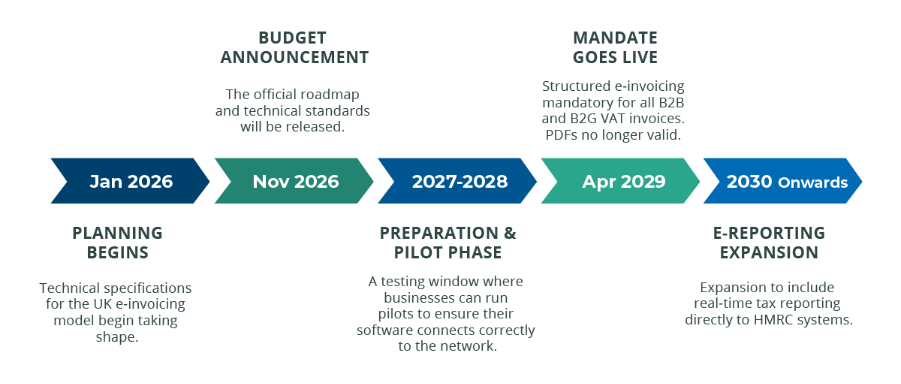

- The Go-Live Date: The UK e-invoicing mandate is set to begin on April 1, 2029.

- The roadmap: A detailed implementation plan will be part of the Budget 2026 announcement. This will give businesses a clear path to follow.

- Software Requirements: You will need e-invoicing software that can both send and receive these data files. Your system must connect to others without you having to type in information manually.

- The MTD Connection: The government is aligning this UK e-invoicing mandate with MTD. This means your invoicing and your tax reporting will eventually live in the same digital ecosystem.

Who is in Scope for the 2029 Mandate?

The mandate applies to all VAT-registered businesses in the UK.

- B2B & B2G Transactions: Business-to-business and business-to-government transactions will require e-invoices.

- Business Sizes: SMEs, mid-market companies, and large enterprises are all included. The government is even looking for low-cost tools to help micro-businesses comply.

- What is Out of Scope? For now, B2C (Business-to-Consumer) transactions are not part of the mandate.

The UK’s E-Invoicing Foundation: Directive 2014/55/EU?

Directive 2014/55/EU is the law that requires public authorities to accept structured digital invoices from suppliers. Unlike MTD, which digitizes VAT reporting to HMRC, this directive digitizes the invoice exchange between buyer and seller.

The UK retained and implemented this directive after Brexit, making it the first formal step toward structured e-invoicing in the UK. The clearest example of this implementation is NHS England. Suppliers to NHS England already submit invoices electronically via the Peppol network using the Peppol BIS 3.0 format, following the EN 16931 standard.

This matters for the 2029 mandate because it shows the upcoming model works. The infrastructure, the standards, and the network are already live and functioning in the UK public sector (B2G). The 2029 B2B mandate is not starting from scratch. It is extending a framework that NHS suppliers have been operating under for years.

The UK E-Invoicing Mandate Timeline: A Complete Roadmap to 2029

Here is the official timeline for the UK e-invoicing mandate:

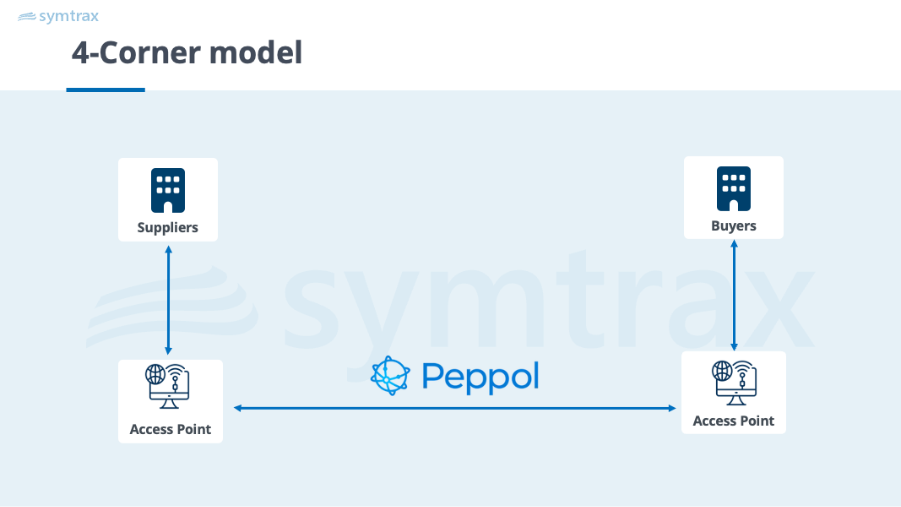

The Model Behind the Mandate: The Decentralized “4-corner” Model

For the 2029 mandate, the UK government has chosen a decentralized 4-corner model. There is no government portal where all invoices must pass through. Instead, businesses exchange invoices directly through their own software providers, connected via a shared network. While no technical standard has been confirmed yet, Peppol has been referenced as the likely framework for exchange.

The UK e-invoicing mandate is built around the decentralized 4-corner model, but it is not the only architecture businesses use today. See how 2, 3, 4, and 5-corner exchange models compare and what each means for your setup.

How to Prepare for the UK E-Invoicing Mandate Before 2029

The 2029 mandate is a few years away. The preparation behind it starts today. Evaluating your current process now gives you the time to act without the pressure of a countdown.

- Assess your current invoice process. Map exactly how invoices are sent and received today. Identify every manual step in between.

- Quantify your pain points. Measure processing times, error rates, and late payment frequency.

- Check your software capability. Review whether your accounting or ERP system already supports structured e-invoicing or connectors to networks like Peppol.

- Talk to your vendor. Ask directly about their roadmap for the 2029 mandate.

- Plan for interoperability. If you trade internationally, make sure your e-invoicing solution supports multiple region formats along with upcoming UK e-invoicing regulations.

- Run a controlled pilot. Test end-to-end with a small group of trading partners before rolling out across your full network.

Future-Proof Your E-Invoicing with Symtrax

The 2029 UK e-invoicing mandate is not just a compliance deadline. It is an opportunity to modernize how your entire business sends, receives, and processes invoices across both AP and AR.

The Compleo Invoice Platform (CIP) is built for exactly this transition. As a proven e-invoicing solution already supporting global e-invoicing mandates across multiple markets, CIP integrates with your ERP and automates your entire invoice life cycle.

[Contact us today] to learn how Symtrax can future-proof your e-invoicing process and make compliance effortless.

FAQs

Starting from April 1, 2029, any UK business registered for VAT will be legally required to send and accept structured electronic invoices. This new rule applies to both business-to-business (B2B) and business-to-government (B2G) sales. PDFs, Word files, and scanned images will no longer qualify as compliant VAT invoices under the mandate.

No. MTD requires digital records and submissions of VAT returns. E-invoicing digitizes the transaction underneath it. They are separate but connected layers of the same digital tax strategy.

E-invoicing refers to the structured exchange of invoice data directly between business systems. E-reporting refers to submitting transaction data in real time to HMRC

Peppol BIS 3.0 and the EN 16931 are widely used and expected to form the basis of the standard, with final technical specifications due at Budget 2026.

No. The mandate does not currently extend to B2C transactions.

No. E-reporting is not part of the 2029 mandate. Real-time reporting of transaction data to HMRC is planned for 2030 onwards.